IRMAA: Stop Overpaying for Medicare and Save Thousands of Dollars

If you’re a high-income retiree approaching 65, beware. Medicare could charge you hundreds of dollars extra per month, unless you plan ahead.

This surcharge is called Income-Related Monthly Adjustment Amount (IRMAA), and it causes many well-off retirees to overpay for Medicare without realizing it. In this article, I’ll explain what IRMAA is, why it catches people off guard, and how you can avoid paying more than necessary. A few smart moves could save you thousands in lifetime Medicare premiums, so read on and take action before you enroll!

What Is IRMAA and Who Pays It?

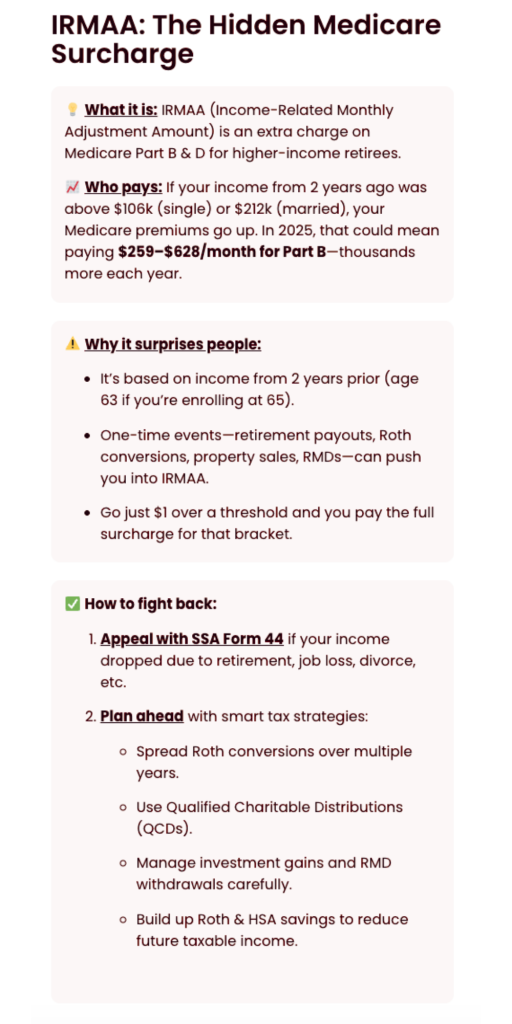

IRMAA is an added premium surcharge for Medicare Part B: medical insurance, and Part D: prescription drug coverage, that high-income earners must pay.

Think of it as a Medicare tax on success: if your income is above certain levels, Medicare charges you more for the same coverage.

How much more? That depends on your income bracket. For example, the standard Part B premium in 2025 is $185.00 per month. But if your modified adjusted gross income (MAGI) from two years prior was above $106,000 if single or $212,000 if married, you’ll pay $259.00 per month for Part B instead.

The surcharges increase at higher incomes

Someone with income in the top bracket, over $500k single or $750k joint, will pay $628.90 per month for Part B. Yes, you read that right: high earners can pay over $6,000 more per year for Medicare Part B than average-income folks. And that’s just Part B. Part D drug plans also have IRMAA surcharges ranging from an extra $13.70 up to $85.80 monthly in 2025, that’s on top of your regular plan premium.

Why does IRMAA exist?

Medicare began charging higher premiums to wealthier beneficiaries in 2007 for Part B and 2011 for Part D. Only about 8% of Medicare beneficiaries have to pay IRMAA surcharges, but if you end up in that group, it can significantly increase your healthcare costs. Importantly, IRMAA is a “cliff” surcharge.

Go $1 over the income threshold, and you’ll pay the full surcharge for that bracket.

There’s no gradual phase-in. In fact, just one dollar of income above the limit would mean paying around $888 extra for Part B and $164 extra for Part D over the year. Clearly, it pays to keep your income within the right limits when possible!

How IRMAA Can Sneak Up on You

You might be thinking, “I won’t have a high income in retirement, so I’m safe.” But IRMAA has a way of surprising even careful planners. Remember, it looks at your income from two years ago. If you’re about to enroll in Medicare at 65, Social Security will check what your income was at 63 from your IRS tax return. Did you have a one-time spike in income that year? Many people do, often unintentionally:

Retirement payouts or severance

Perhaps you retired at 63 and took a severance package or cashed out unused vacation. That could have pushed your income above the IRMAA threshold for that year. Two years later, Medicare will still charge you extra, even if your current income is much lower.

Large IRA withdrawals or Roth conversions

Converting a chunk of your traditional IRA to a Roth, or withdrawing a large amount for a big purchase, can increase your MAGI and trigger IRMAA. In fact, large Roth conversions are a common reason retirees get hit with IRMAA, according to financial planners.

Capital gains from investments or property

Did you sell a rental property, business, or a stock portfolio for a profit? A capital gain beyond the usual amount, for example, a home sale with gains above the $250k/$500k tax-free limit, can boost your MAGI in that year. Even mutual funds can distribute taxable capital gains that increase your income unexpectedly.

Required Minimum Distributions (RMDs)

Once you hit age 73 you must start withdrawing from traditional IRAs/401(k)s. Those withdrawals count as income. A large IRA balance can produce RMDs hefty enough to push you into IRMAA territory if you haven’t planned for it.

The frustrating part is that if your income spike was just a one-year event, IRMAA still charges you for a full year of higher premiums. There is no automatic adjustment to say “this was a one-time thing.” Social Security will re-check each year with a two-year lookback, so the good news is the surcharge might disappear the following year if your income drops back down. But that’s cold comfort after you’ve already paid an extra few thousand dollars in premiums for a year.

The key is to anticipate these triggers before they happen or address them immediately if they do.

Two Ways to Avoid Overpaying for Medicare

The best approach to IRMAA is a two-pronged strategy: appeal if you qualify, and plan ahead to minimize future surcharges. Here’s how:

1. Appeal IRMAA if Your Income Dropped (Life-Changing Event)

If you get an IRMAA surcharge notice but your current income is lower than it was two years ago due to certain life events, you may be in luck. The Social Security Administration (SSA) allows you to request a reduction in your Medicare premium if you’ve experienced a “life-changing event” that cut your income. What counts as life-changing? According to SSA, eligible events include: retirement or work stoppage, cutback in work hours, marriage, divorce, death of a spouse, loss of income-producing property, loss of a pension, or receiving a settlement from an employer such as severance. For example, if you or your spouse retired recently and your income for this year is far below what it was two years ago, that’s a valid reason to appeal.

To appeal, you file Form SSA-44 or the Medicare IRMAA Life-Changing Event form with documentation of your situation. You’ll need to show proof of the event like a letter from your employer about your retirement, a divorce decree, or death certificate, etc. You’ll also need evidence of your new lower income such as a recent tax return or an estimate of your current year income.

If approved, SSA will adjust your Part B and D premiums downward, often eliminating the IRMAA surcharge entirely. This can save you hundreds of dollars per month going forward, and sometimes you even get a refund for past overpayments. It’s worth the effort: one retiree described how carefully following the appeal process resulted in premiums dropping by $70/month and an $800 refund for prior overcharges.

Pro Tip: If your IRMAA appeal is denied because SSA says your situation doesn’t meet their listed events, you can pursue further appeals up to a Medicare Appeals Council and even federal court. However, appeals beyond the initial SSA-44 are rarely successful unless a qualifying event truly exists. Generally, if your high income was purely from a one-time financial transaction like sale, large investment gain, etc., SSA will not waive the surcharge. In that case, focus on future prevention instead.

2. Plan Ahead to Prevent IRMAA Surcharges

The second way to beat IRMAA is by proactive income planning. This is where you can truly save yourself a lot of money and headache by making strategic moves before you cross an IRMAA threshold. Here are some trusted strategies financial advisors recommend to keep your income under IRMAA limits:

Time Your Roth Conversions and Withdrawals

Converting traditional IRA funds to a Roth IRA can be smart long-term, but do it in small chunks. Roth withdrawals in retirement aren’t counted as income for IRMAA. Spreading a conversion over several years helps ensure you don’t spike your income in any single year. Similarly, if you need funds for a large expense, consider breaking the withdrawal into two tax years or other financing such as a short-term loan to avoid a one-year income jump that triggers IRMAA.

Maximize Tax-Free and Tax-Deferred Accounts

While you’re still working, contribute as much as possible to your 401k, 403b, traditional IRA, or other tax-deferred plans. Every dollar you keep out of your taxable income helps keep your MAGI down. Also remember, Roth IRAs and Health Savings Accounts (HSAs), if eligible, grow money that won’t count toward your MAGI in retirement. Building up these accounts means you can pull money in retirement without increasing your IRMAA exposure.

Use Qualified Charitable Distributions (QCDs)

If you’re over 70½, you can donate directly from your IRA to charity up to $100,000 per year. This QCD counts toward your RMD but doesn’t count as income on your tax return. It’s a great way to reduce taxable income, and thus MAGI if you intend to give to charity anyway. Lower MAGI could keep you below an IRMAA tier and save you money in premiums.

Manage Investment Gains

Keep an eye on capital gains in your taxable investment accounts. If you had a big gain like you sold some stocks at a profit, see if you have losses to harvest to offset those gains. And if your mutual funds are throwing off large capital gain distributions each year, it might be time to switch to more tax-efficient funds or ETFs to avoid unexpected income boosts.

Every situation is unique. The main idea is to be mindful of actions that inflate your MAGI. Sometimes taking a large income hit might be worthwhile. For instance, doing a substantial Roth conversion in a low tax year, even if it triggers one year of IRMAA, could save more in the long run. The key is to make that decision consciously, with full awareness of the cost, rather than getting blind-sided by a surcharge letter later.

This is where working with a knowledgeable financial planner or Medicare specialist is invaluable. They can run “IRMAA what-if” scenarios and craft a plan so that you keep more of your money over the course of your retirement.

How Katie Diemer Can Help You Save on IRMAA

Navigating IRMAA can be complex, but you don’t have to figure it out alone. Katie Diemer specializes in helping higher-income individuals minimize Medicare costs. I stay up-to-date on the latest IRMAA brackets and regulations, and I know the ins and outs of appeals and strategic planning. I take a personalized approach: analyzing your income sources, tax situation, and retirement goals to identify the best steps for you.

Imagine keeping an extra $3,000, $4,000, or even $6,000 in your pocket each year instead of handing it over in Medicare surcharges. I’ve helped clients achieve exactly that: from successfully filing IRMAA appeals that erase unwarranted charges, to executing tax-efficient income strategies that prevent IRMAA altogether. The result is often immediate savings on Medicare premiums and the long-term satisfaction of knowing you won’t be ambushed by surprise costs.

Ready to take action?

If you’re approaching 65, or already on Medicare, and have a higher income, now is the time to plan. Don’t wait until an IRMAA letter shows up in your mailbox. Contact Katie Diemer for a free IRMAA consultation or try our IRMAA Impact Test to see where you stand. I’ll help you chart a course to avoid overpaying Medicare. Your retirement dollars are precious. Let’s make sure they’re working for you, not wasted on unnecessary premiums.

By being proactive and informed, you can enjoy your Medicare benefits without the IRMAA hassle. Remember: IRMAA is not a given. It’s a cost you can control with the right guidance. Let Katie Diemer show you how to keep your hard-earned money and health coverage in perfect balance.

I’m here to help! Schedule your free call today

Take the next step toward a stress-free Medicare experience. I’m here to help you make sense of Medicare, so you can move forward to this new chapter with peace of mind and confidence in your health coverage.