Turning 65 soon and feeling unsure about Medicare? You’re in the right place.

Navigating Medicare can seem daunting, but it doesn’t have to be. In this guide, I’ll break down the basics of Medicare in clear, simple terms. My goal is to answer common questions like “What are the different parts of Medicare?” and “When do I need to sign up?”. All so you can make informed decisions about your health coverage.

By the end, you’ll understand the key things Medicare covers and doesn’t cover, what choices you’ll have to make, and how to take your next steps with confidence.

What Is Medicare and Who Is It For?

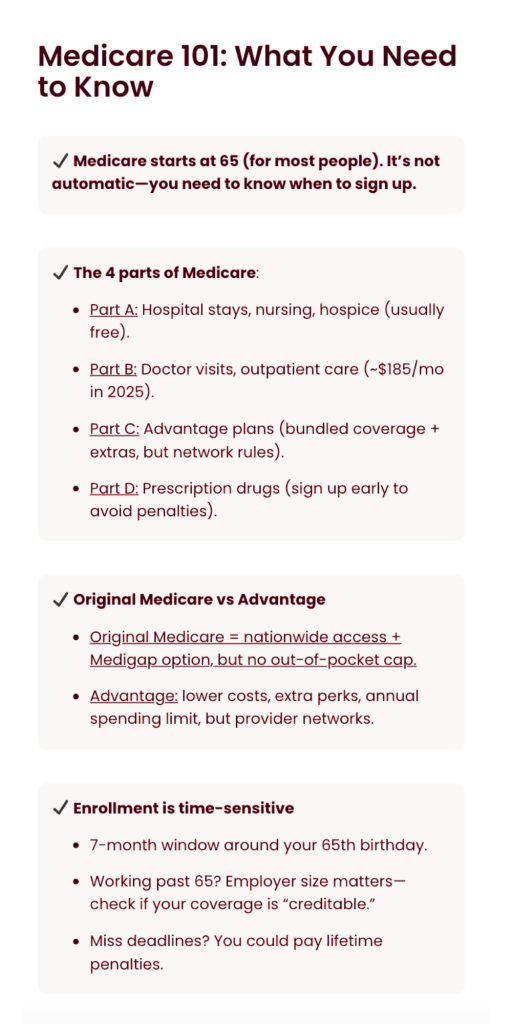

Medicare is the United States government’s health insurance program for people aged 65 and over. It also covers some younger individuals with certain disabilities or serious diseases, but for most folks, Medicare kicks in when you turn 65. Think of Medicare as a safety net to help with hospital bills, doctor visits, and more once you’re eligible. However, Medicare isn’t automatic for everyone, and it has multiple “parts” that each cover different things.

Let’s start with an overview of those parts, since they’re the building blocks of understanding your Medicare options.

The Four Parts of Medicare: A, B, C, D

Medicare is divided into four main parts, each designated by a letter. Here’s a quick rundown of what each part covers:

Part A (Hospital Insurance)

Helps pay for inpatient hospital stays, rehabilitation in a skilled nursing facility, hospice care for the terminally ill, and some home health care. Part A is often premium-free for most people because you (or your spouse) paid Medicare taxes while working. In short, Part A is your coverage for hospital room, board, and related inpatient services.

Part B (Medical Insurance)

Covers most of your routine medical needs: doctor’s appointments, outpatient surgery, lab tests, preventive screenings like mammograms or colonoscopies, mental health counseling, and durable medical equipment (think wheelchairs or oxygen tanks). Part B does have a monthly premium, which is approximately $185 in 2025 for most beneficiaries. After a small annual deductible, Part B generally pays 80% of covered services, and you pay the remaining 20%.

Part C (Medicare Advantage)

An alternative way to get your Medicare benefits through private insurance companies. Medicare Advantage plans replace Original Medicare (Parts A and B) with a bundled plan that at minimum covers everything Original Medicare does, and often includes extras like prescription drug coverage, dental, vision, or hearing benefits. These plans usually have networks of doctors and hospitals you’ll use, similar to an HMO or PPO. You still have to be enrolled in Parts A and B to join Part C, and you’ll continue to pay your Part B premium. Many Advantage plans have low or even $0 additional premiums, making them an attractive option for cost-conscious consumers, but you’ll trade some flexibility for that convenience. More on this trade-off below.

Part D (Prescription Drug Coverage)

This part helps pay for your prescription medications. You can get Part D by enrolling in a standalone Medicare Part D drug plan or through a Medicare Advantage plan that includes drug coverage. Every Part D plan has a list of covered drugs (a formulary), and it will typically cover both generic and brand-name medications that you get at the pharmacy.

Like other insurance, Part D plans have monthly premiums and cost-sharing. Cost-sharing here means copays or co-insurance for your meds. Importantly, if you don’t sign up for drug coverage when you’re first eligible and you go without other credible drug insurance, Medicare may charge you a late enrollment penalty if you decide to get Part D later.

So even if you don’t take many prescriptions now, it’s wise to have at least some form of drug coverage when you start Medicare.

Original Medicare vs. Medicare Advantage: How Do They Differ?

When you first enroll, one of your biggest decisions will be whether to:

- Stick with Original Medicare: Parts A & B, usually paired with additional coverage, or…

- Choose a Medicare Advantage plan: Part C.

Both paths can cover you, but they work differently. Here’s a comparison to clarify:

Original Medicare (Parts A & B + optional add-ons)

With Original Medicare, you can visit any doctor or hospital nationwide that accepts Medicare, no network limitations. Medicare pays its share of the bill, and you pay the rest. Because there’s no annual cap on your out-of-pocket costs in Original Medicare, many people purchase a Medicare Supplement (Medigap) policy to cover things like the Part A hospital deductible and the 20% coinsurance under Part B. If you go this route, you’d also likely add a Part D drug plan for prescriptions, since Original Medicare doesn’t include drug coverage.

This combination (A + B + Medigap + D) offers very comprehensive coverage and maximum choice of providers. The trade-off is you pay separate premiums for Part B, a Medigap plan, and Part D. This can sometimes cost more monthly than an Advantage plan. However, Medigap can greatly reduce or eliminate your out-of-pocket expenses when you get care, and you won’t need referrals to see specialists.

Medicare Advantage (Part C) Plans

With Medicare Advantage, a private insurance company provides all your Part A and Part B coverage, and usually Part D as well, in one neat package. These plans often have lower upfront costs, many have low or $0 additional premiums beyond your Part B premium. They also put an annual limit on what you pay out-of-pocket for medical services, which Original Medicare alone does not. On top of that, Advantage plans can include perks like dental cleanings, eyeglasses, hearing aids, gym memberships, or other benefits that Original Medicare doesn’t cover.

The trade-offs to Medicare Advantage? You typically must use doctors and hospitals within the plan’s network (for non-emergency care) to get the lowest costs. You might need referrals to see specialists, depending on the plan. And costs like copays can apply each time you see a doctor or receive a service (as opposed to Medigap, which can cover those costs entirely). Medicare Advantage plans can vary a lot, some mimic HMOs, others PPOs, so it’s important to compare plans in your area on things like provider networks, drug coverage, and out-of-pocket maximums.

If you ever decide an Advantage plan isn’t for you, you can switch back to Original Medicare. This is usually only during certain enrollment periods, unless you qualify for a special exception.

Which option is better?

That truly depends on your individual needs, budget, and preferences. Some people value the wide choice of providers and predictable costs that Original Medicare with a Medigap provides. Others prefer the simplicity and extra benefits of a Medicare Advantage plan.

There’s no one-size-fits-all answer, but understanding the differences is the first step. As you approach 65, it’s a great idea to talk with a Medicare advisor (like us at KRS) who can walk you through the specifics and help determine which route aligns with your health and financial situation.

When and How to Enroll in Medicare

Timing is critical when it comes to Medicare enrollment. Most people have an Initial Enrollment Period (IEP) when they first become eligible for Medicare. If you’re qualifying by age (65), your IEP is a 7-month window: it begins 3 months before the month you turn 65, includes your birth month, and ends 3 months after that month. For example, if your 65th birthday is in June, your enrollment window runs from March 1 through September 30.

Enrolling early in the first 3 months of your IEP is often wise: it ensures your Medicare starts as soon as you turn 65. Enrollments during the later part of the window can sometimes have a delayed start date for Part B.

How to sign up

If you’re already receiving Social Security benefits before 65, here’s some good news: you’ll be automatically enrolled in Medicare Parts A and B starting the first day of the month you turn 65. In which case your Medicare card will arrive by mail. However, if you’re not yet drawing Social Security, you’ll need to actively sign up.

You can apply for Medicare online at the Social Security Administration’s website, or by calling or visiting a Social Security office. It’s a simple application. Remember, even if you’re delaying Social Security retirement benefits, you can and often should still enroll in Medicare during your IEP.

What if you’re still working at 65?

Many people today don’t retire right at 65. If you plan to keep working and have health insurance through your employer (or your spouse’s employer), you may be able to delay taking Part B, and avoid its premiums, until you retire or lose that coverage.

There are Special Enrollment Periods (SEP) for situations like this. As long as your employer coverage qualifies, you can sign up for Part B later during an 8-month SEP after your employment or coverage ends, without incurring late penalties. Always double-check with your employer benefits office to see how your insurance works with Medicare. For example, companies with 20 or more employees typically let you postpone Medicare Part B because their group plan remains primary for you at 65.

But if your company is small, Medicare might become primary at 65, meaning you should enroll in Part B on time. It’s a good idea to get confirmation in writing of your coverage’s creditable status for both medical and drug coverage, just to protect yourself from penalties later.

Beware of late enrollment penalties

If you don’t have other qualifying coverage and you skip Part B or Part D during your initial window, Medicare can charge you a penalty that permanently increases your premiums when you do eventually enroll.

- The Part B penalty is 10% extra for each full 12-month period you should have had Part B but didn’t, and it lasts for life.

- The Part D penalty is calculated as 1% of the national average premium for each month you delayed enrollment without other drug coverage, also lasting for life.

These penalties are meant to encourage timely enrollment. The bottom line is: know your deadlines and don’t miss them unless you have a valid reason. Valid reasons can be for example employer coverage. If you’re unsure, please reach out for guidance, a quick conversation can save you from costly mistakes.

Next Steps and Getting Help

Making sense of Medicare is a journey, and you don’t have to do it alone. By starting with the basics in this Medicare 101 guide, you’ve taken an important step toward feeling more confident about your healthcare decisions.

As you get closer to 65, you’ll likely have more specific questions like “Should I get a Medigap or an Advantage plan?” or “Which drug plan is best for my medication list?”. That’s completely normal, and that’s where one-on-one guidance can be incredibly valuable.

Our Medicare Specialists are available free of charge

I specialize in helping people just like you navigate Medicare with clear, honest advice. I stay up-to-date with the latest rules, costs, and plan options so we can answer your questions and help you avoid pitfalls.

The best part? Our help costs you nothing. I’m an independent, ethical resource, paid by insurance carriers if you enroll in a plan, so my services come at no charge to you.

Ready to get personalized advice?

In a short conversation, we can discuss your unique situation, explain your options in plain language, and make a plan for your Medicare enrollment. There’s no pressure and no obligation, just answers and support. Click the link below to set up your free consultation at a time that works for you.

I’m here to help! Schedule your free call today

Take the next step toward a stress-free Medicare experience. I’m here to help you make sense of Medicare, so you can move forward to this new chapter with peace of mind and confidence in your health coverage.

Call me at (563) 380-7506.